The signal.

- The quantum computing industry is maturing and moving away from laboratory demonstration into industrialised systems engineering.

- Hybrid AI, HPC and quantum workflows are emerging as the most credible route to near-term value.

- Organisations that build understanding, partnerships and readiness now will be best positioned to benefit as the technology matures.

2026 is emerging as the year the quantum computing industry began transitioning from scientific exploration into industrialised systems engineering. Quantum companies are evolving from research organisations into vertically integrated technology enterprises. These entities are defined increasingly by manufacturing, supply chains, reliability, interoperability and scalable deployment rather than laboratory demonstration alone.

Established big businesses such as IBM, Google Quantum AI and Microsoft have acted to create and support the early stages of the industry. By using their immense resources, these behemoths have established many of the technical and commercial foundations of the industry. They have provided valuable demonstrations of early quantum computing to the world and have established their own internal vertical quantum computing enterprises. But, just as we saw in the 1970s in the classical computing industry, many of the most disruptive advances are now emerging from startups such as PsiQuantum, Pasqal and Silicon Quantum Computing, alongside a rapidly expanding ecosystem of specialist startups.

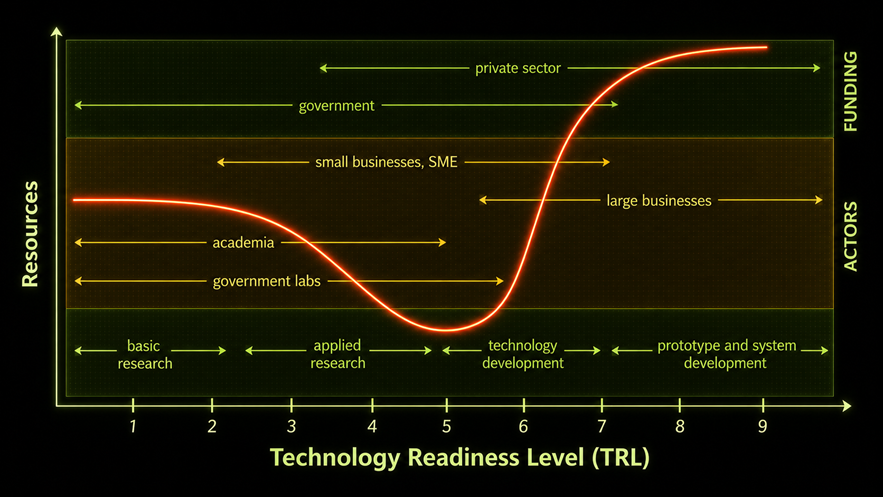

Much of the quantum ecosystem is comprised of start-ups having more in common with university research groups rather than profit-driven enterprises. The reasons for this relate to the relationship between the maturity of the technology being used, who wants to use it, and who provides the resources.

To date, most startups have been immature primarily because the technology readiness level, a measure of how close the technology is to being made into a useful commercial product, is low. This low level of TRL is where academia and government labs are mostly present as they excel in developing new technologies before mass market commercialisation. The companies must fit into that technology-driven environment, which is precisely what we have seen. Many of these organisations were founded by academics and continue to employ large numbers of researchers and early-career scientists.

“ Orbsight has assessed that useful quantum computing will emerge through a gradual transition from scientific demonstration to engineered utility. ”

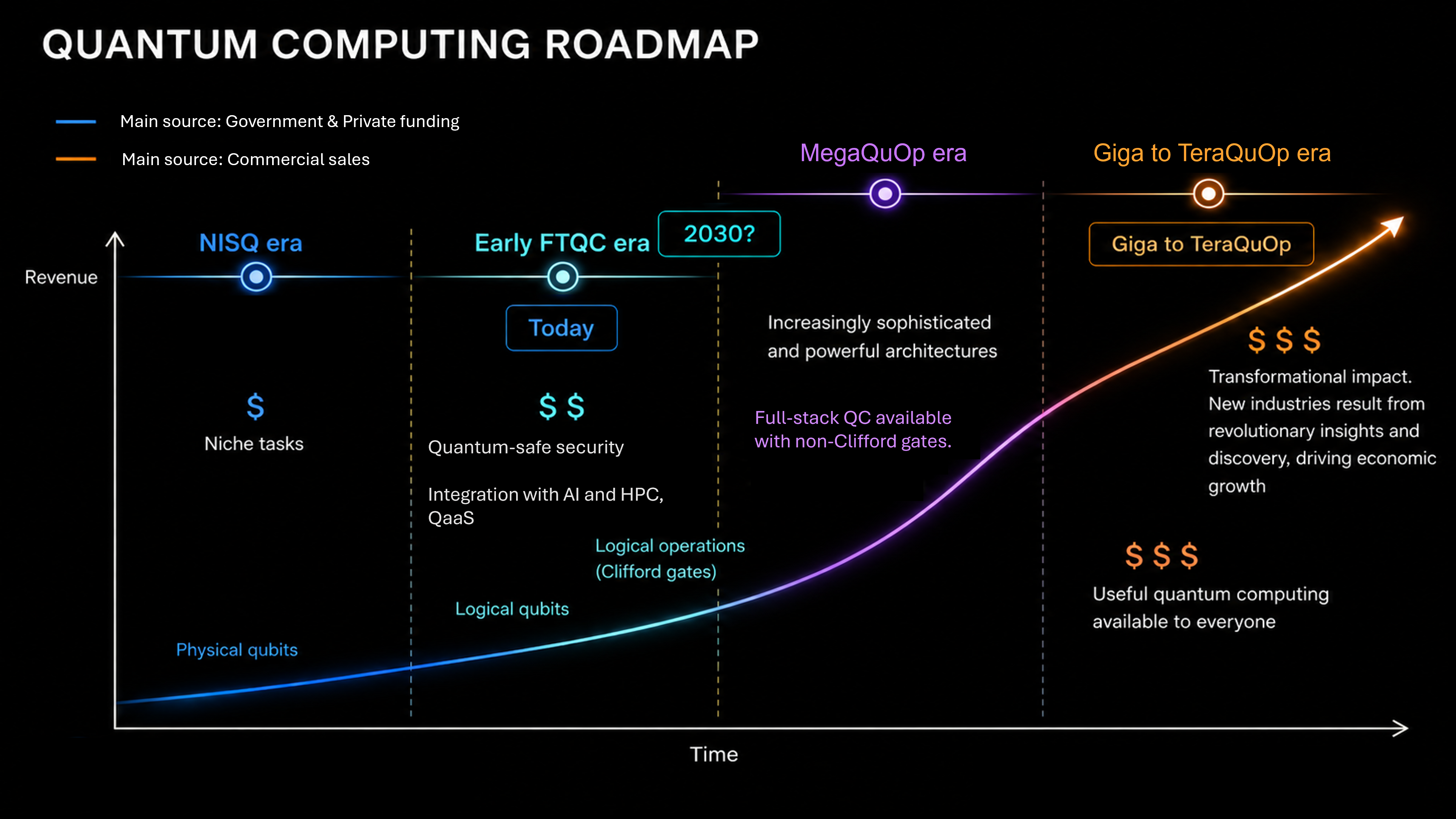

But the period of a startup acting like a research lab who has won the lottery is coming to an end. In recent months, increasing numbers of companies have begun pursuing vertically integrated strategies through fundraising, partnerships and acquisition e.g. Quantinuum, IonQ, SEEQC and IQM. The reasons for this structural change in the industry come from the technological progress being made in the industry, boosting confidence and unlocking further investment. Technological bottlenecks and many risks still exist but the basic roadmap to useful quantum computing using the logical qubit methodology is widely recognised and adopted, shown below.

Fault-tolerant architectures capable of supporting large-scale non-Clifford gate operations are widely viewed as a prerequisite for achieving broad, scalable quantum advantage across many practically important problem classes.

Orbsight has assessed that useful quantum computing will emerge through a gradual transition from scientific demonstration to engineered utility. While fault-tolerant quantum computing remains a major technical challenge, meaningful commercial and strategic value is already beginning to appear through niche applications, hybrid workflows and ecosystem development.

Evidence of commercial value

- Quantinuum working with pharmaceutical and materials companies on molecular simulation workflows.

- D-Wave Quantum reporting optimisation deployments in scheduling, logistics and resource allocation.

Evidence of strategic value

- EuroHPC integrating systems from companies such as IQM.

- CESGA, Julich, RIKEN, NQCC and other national facilities fostering early quantum computers.

- Governments targeting quantum as a strategic infrastructure e.g. UK £2B+ quantum commitments, EU fabrication initiatives, USA DARPA's Quantum Benchmarking Initiative, India's quantum workforce programmes.

- Financial-sector quantum-safe planning.

Many of the current bottlenecks increasingly appear solvable through engineering iteration rather than entirely new scientific discovery. This does not eliminate risk, but it suggests many of the remaining challenges are increasingly engineering problems rather than fundamental scientific barriers.

“ Many of the remaining challenges in quantum computing increasingly appear to be engineering problems rather than fundamental scientific barriers. ”

Scaling and manufacturing

Building a few high-performance qubits in a laboratory is very different from reproducibly manufacturing millions of reliable components at scale. Each qubit modality has different scaling challenges but they all must solve yield, packaging, stability, control complexity, operational throughput. Possible solutions include semiconductor-style process control, automated calibration, improved fabrication metrology, modular architectures and co-design between hardware, software and manufacturing teams. Long-term success will depend as much on industrialisation discipline as on scientific breakthroughs.

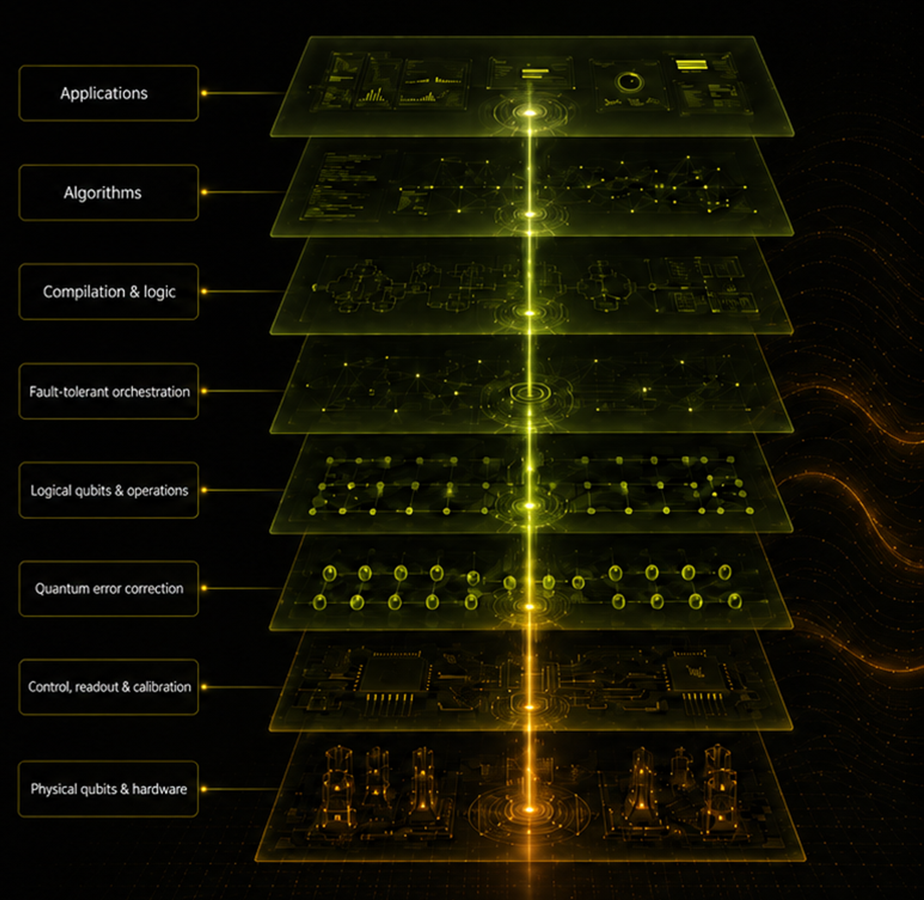

Control and fault tolerant middleware

Control, quantum error correction, logical qubits and operations, fault tolerant orchestration and compilation, and logic stacks form the middleware of a quantum computer. These stacks are classical computers. The large number of physical qubits generate enormous volumes of syndrome data requiring ultra-fast decoding, feedback and control decisions. Latency, bandwidth and hardware orchestration are now major engineering bottlenecks. The control systems must operate as real-time companions to the qubit hardware. Possible solutions include specialised CPU, FPGA and GPU architectures, distributed control architectures, improved decoder algorithms and standardised software interfaces between hardware and QEC layers.

Quantum algorithms and applications

Quantum computers will only be economically valuable if they can run algorithms that solve important problems better than available classical approaches. Many quantum algorithms remain unproven at practical scale. End-users increasingly seek realistic assessments of where quantum computing may outperform classical methods rather than theoretical demonstrations alone. Industries such as finance, chemistry, materials science and logistics continue exploring opportunities, but uncertainty remains around performance advantages and integration costs. A major challenge is matching quantum hardware capabilities with problems that tolerate the limited qubits available in a typical QPU today. Possible solutions include hybrid quantum-classical workflows, application-specific optimisation, improved benchmarking and closer collaboration between domain experts, software developers and hardware providers to identify achievable near-term value while preparing for better large-scale fault-tolerant systems.

Integration with AI and HPC

Quantum computing is unlikely to operate in isolation and will instead emerge as part of broader hybrid computing infrastructures alongside AI and HPC. Quantum systems currently rely heavily on classical compute resources for orchestration, simulation, optimisation and error correction. Integrating these technologies introduces challenges around software interoperability, data movement, scheduling and workflow management. Organisations must also determine where quantum acceleration genuinely improves performance rather than adding unnecessary complexity. Possible solutions include unified software frameworks, cloud-native orchestration platforms, AI-assisted calibration and optimisation tools, and tighter integration between quantum processors and HPC environments. Hybrid AI, HPC and quantum architectures are increasingly viewed as the most likely route to practical quantum value over the coming 5 years.

Summary

The quantum computing industry is entering a new phase of industrial maturation. In 2026 we see that the future of quantum computing will be built not only through advances in qubits, but through the integration of fault tolerant architecture, manufacturing, classical HPC, AI and deep-tech product development. Quantum is moving from research promise to systems integration. However, timelines remain uncertain, some companies will fail, consolidation is likely as found in any industry making this type of transition, scalability is not guaranteed, and practical value will almost certainly emerge unevenly. The long-term potential value of quantum computing remains substantial, although the scale and timing of that value are still uncertain. Already we are seeing meaningful value emerging through niche applications, quantum-safe security initiatives and strategic positioning within emerging quantum supply chains. At the same time, organisations are investing in AI, HPC and quantum integration to prepare for future hybrid computing architectures.

Organisations should begin preparing now rather than waiting for fully fault-tolerant quantum computing to arrive. The emergence of a conventional quantum industry changes the nature of engagement from speculative research to strategic capability development. Businesses should identify potential use cases, monitor ecosystem developments, assess quantum-related risks such as cryptographic vulnerability and build internal awareness. Early engagement does not require major investment, but it does require understanding where quantum technologies may create competitive advantage over the coming 5 years.

For qubit builders

Build your vertical stack offering by partnering with the best suppliers of middleware, quantum algorithms and applications

For investors

Identify the organisations that can industrialise their technology

For adopters

Become ready for quantum's disruptive opportunities

About Orbsight

Orbsight helps organisations separate signal from hype while preparing for the transition toward useful quantum computing.

Drawing on experience across quantum device design and manufacture, miniaturised instrumentation, quantum error correction and deep tech commercialisation, Orbsight connects research, industry and investment with clear-eyed insight, technical credibility and a focus on real progress over hype. Orbsight provides services that include:

- Quantum architecture and manufacturing advisory

- Fundraising and investment strategy

- Quantum readiness assessments

- Integration strategies

- Ecosystem and partnership insight

Next move

Bring clarity to your next quantum computing decision. Whether you need to understand, invest, partner, build, integrate, communicate or wait, Orbsight will help turn that uncertainty into a practical route forward.